Every day we hear “blockchain” is solving another of the world’s problems. Here are some highlights from 2017 so far;

- February 27th – Sweden tests blockchain technology for land registry

- March 6th – United Nations World Food Programme Uses Blockchain Technology to Alleviate Hunger

- March 24th – Alibaba to use blockchain to fight China’s fake food

- April 26th – Spotify acquires Blockchain start up Mediachain to solve music’s attribution problem

- May 22nd – Toyota pushes into blockchain tech to enable the next generation of cars

- May 28th – Stopping Fake News: DNN Uses the Blockchain for Factual Reporting

Its being claimed that Blockchain will enable the next generation of cars? It can help artists get their royalties? It can help alleviate world hunger? And it can stop Donald Trump’s biggest problem – Fake news!?

What is going on? What is this blockchain thing and how can it apply to such a wide range of problems? My aim is to answer this question and help you understand more about this illusive technology. Granted, it is hard to understand, so I encourage you to do research of your own. We are in the early days of this technology, the best is yet to come so now is the best opportunity to get involved.

Blockchain is to Silicon Valley what Silicon Valley is to the rest of the world

A brief history of Bitcoin (the first blockchain)

In late 2008, a white-paper1 detailing Bitcoin was first released by the alias “Satoshi Nakamoto”. I say alias as the true identity of this person/people is still not known. Some say this was the internet’s response to the global financial crisis as it tackled head on the high degree of trust we place in financial institutions to hold our money safely. It was built upon the idea that banks are not needed to hold our money or facilitate transactions. Satoshi argued we should instead place our trust in computer code that uses complex cryptography alongside a globally distributed & public computer network which processes transactions. The network acts as a single entity to guarantee the authenticity of the payment. The result – Bitcoins could be transferred anonymously & securely to anyone, without banks, without regulation, not bound by any anti-money laundering protections or treaties. All ‘payments’ were sanctioned which represented an ‘off the grid’ system.

The first Bitcoin computers came online early 2009. In the early days each ‘Bitcoin’ had a value of 9 Australian cents. Fast forward and today, each Bitcoin is valued at $3450 with a global network of 7,000 nodes across 87 countries shifting $1.9 Billion around the globe every day. Whilst these numbers are tiny when compared to other payment networks like SWIFT2 or Visa, they are growing at a very quick rate.

Its reliance on “cryptography” and it being a “currency”; Bitcoin (and many others) are referred to as a “crypto-currency”. As of writing there are 700+ crypto-currencies in circulation.

So how does it work?

Behind Bitcoin lies the blockchain, the technology that makes it work. It allows people to create their own bank accounts or digital wallets as they are called. These wallets have two key components:

A “shared key” which is what you give to others to send Bitcoins to you. An example is “1J8rqPAXQ483P7jQXJpEXb19Dg9GsknXDZ”

A “secret key” which is what you use to create transactions from your wallet and send Bitcoins to other people. An example is “KxZzUACnAubkfSKen8ZNN7UKQcuE9LqdEFCpoamHUsK1eyqMmpU7”

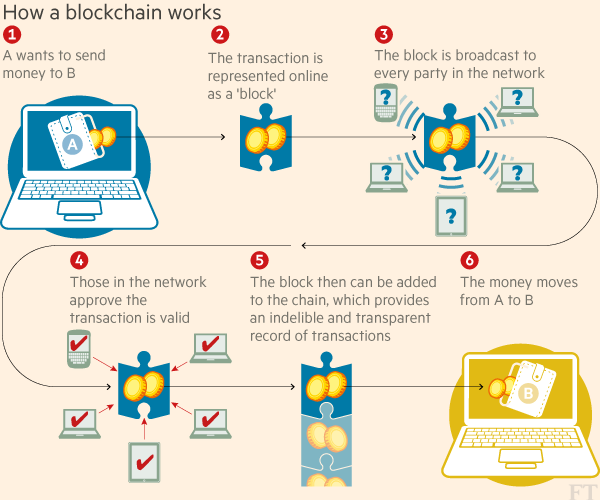

We then use these two components to perform transactions. Check the following image as it shows the sequence:

Courtesy of Weforum

It’s these blocks of transactions that are sent around the world and stored on multiple computers, as more blocks are created they are added to the chain, which in turn forms the blockchain. Inside are the records (or ledger) of all transactions and since all members on the network need to validate the transaction, there’s thousands of computers around the world that have a record of it. People who run these computers are incentivised to process these transactions by being given a small fee, just like those annoying credit card fees except these are far smaller. You can actually use your home computer to process these transactions and earn your own Bitcoin.

You don’t just have access to parts of a transaction, like when you transfer money to your friends bank account, you only see money leaving your account, you don’t get a verification advising the person has received it. This is due to the centralised nature of the current banking system. The ledger of transactions is centralised. In this case, the central computer keeps a log of what has moved where. With blockchain, the ledger is distributed across all computers on the network and the end-to-end transaction record is there for you to see.

How secure is it?

With the public distribution of the ledger, everyone can see transactions and see how much value is in your wallet. Imagine going into a bank vault and being able to see into all the deposit boxes but, not having the keys to open them and not knowing who owns them.

Courtesy of BlockChain Explorer

Above we can see a single transaction of 1.09 bitcoin from one wallet to another. I don’t know who owns both wallets though I can see the transaction. A hacker would have to break a SHA256 code, which is so secure the NSA, FBI & CIA uses it to encrypt their data. Alternatively, a hacker could gain control of 51% (or 3500) of all computers on the globally distributed & encrypted network to adjust the ledger manually. As improbable and unrealistic as this sounds, protections have been built into the platform to prevent this type of attack. This is why it’s so important people guard their digital-wallets ‘secret key’ which is the easiest way to hack the system – get a copy of your secret key and perform a ‘legitimate’ transaction on the network. It’s just like having the wallet in your pocket stolen and seeing a transaction you did’t make appear on your statement.

How many ‘blockchains’ are there?

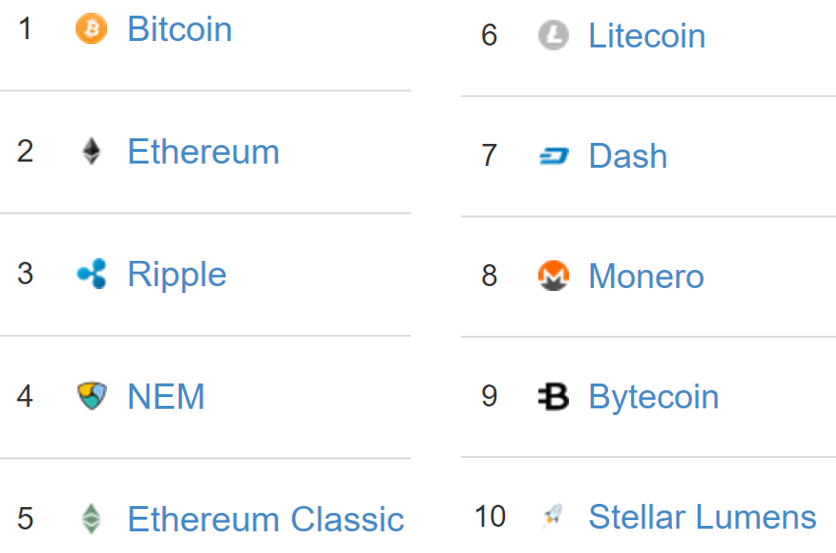

Bitcoin is not the only blockchain, but one of many in existence. As of writing approximately 700 public blockchains3 are operating around the world, each with their distinct features, scale & use. The ‘top 10’ include:

Courtesy of CoinMarketCap

Moving towards a trust-less system

Our society is built on trust. We trust our banks to hold our money. We trust our governments to spend our tax dollars. We trust our supermarkets stock reliable products. We even trust Spotify to pay artist royalties – Spotify is actually being sued for not paying royalties. Blockchain helps

- Helping deliver aid: Aid is best served not by giving impoverished areas food but by providing them with the tools needed to grow and sustain food supplies by create micro economies in these areas. The World Food Programme uses a blockchain to make it quicker, easier, less riskier & less costly than traditional methods to deliver aid in this way.

- Stopping Fake News: Having trace-ability to the source of news can validate where information comes from. Through a blockchain, readers can validate this instantly rather than trusting the media outlet to be unbiased.

- Stopping Fake food: Eliminating counterfeit food products tracing the source of ingredients as they move through the supply chain. Why trust a sticker that says organic when you can track where it came from?

- Artist Royalties: Would you feel more comfortable seeing that your favourite artist was compensated that time you listened to their song rather than trusting Spotify to pay them? Blockchain is the mechanism to validate artists are compensated when their track is played.

These are just some use cases. Hopefully you are now a little more aware of what blockchain is and why it is so relevant. Every day more of the world’s problems are being tackled head on by blockchain. In my view, it’s not just another technology looking for a problem, it represents a grand opportunity for us to make large-scale structural change in a positive way.

1 – Bitcoin: A Peer-to-Peer Electronic Cash System

2 – SWIFT Traffic Figures

3 – Coinmarketcap.com List of Crypto-currencies